Equity Proves to Be a Game-Changer for Homeowners Seeking to Sell

If you’re a homeowner, you might be torn on whether or not to sell your house right now. Maybe that’s because you don’t want to take on a higher mortgage rate on your next home. If that’s your biggest hurdle, understanding your equity may be exactly what you need to help you feel more comfortable making your move.

What Equity Is and How It Works

Equity is the current value of your home minus what you owe on the loan. And recently, that equity has been growing far faster than you may expect.

Over the last few years, home prices rose dramatically, and that gave your equity a big boost very quickly. While the market has started to normalize, there’s still an imbalance between the number of homes available for sale and the number of buyers looking to make a purchase. And it’s because homes are in such high demand that prices are back on the rise today. Rob Barber, CEO of ATTOM, a property data provider, explains:

“Equity levels were high even during the recent downturn, and now they are going back up and better than ever.”

How Equity Benefits You in Today’s Market

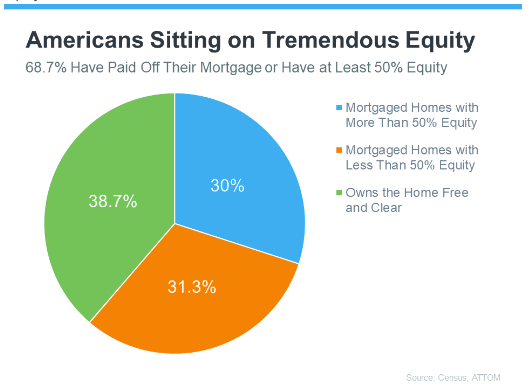

With today’s affordability challenges, that equity can be a game changer when you move. Here’s why. Based on data from ATTOM and the Census, nearly two-thirds (68.7%) of homeowners have either paid off their mortgages or have at least 50% equity (see chart below):

That means roughly 70% have a tremendous amount of equity right now.

Once you sell your house, you can use your equity to help with your next purchase. It could be some (if not all) of what you’ll need for your next down payment. It may even be enough to allow you to put a considerably larger down payment on your next home, so you don’t have to finance quite as much. And, if you’ve been in your current house for years, you may have even built up enough equity to pay in all cash. If that’s true for you, you’d be able to avoid borrowing altogether, so you wouldn’t have to worry about today’s mortgage rates.

There are two main ways that a homeowner can leverage their home equity to buy a larger home:

1. Home equity loan

A home equity loan is a second mortgage that allows you to borrow against the equity in your home. The amount you can borrow is typically limited to 80% of your home's equity, minus the balance of your first mortgage. Home equity loans are typically repaid over a fixed term of 5 to 30 years, and have fixed interest rates.

2. Cash-out refinance

A cash-out refinance is a type of refinance that allows you to replace your existing mortgage with a new one that is larger. The difference between the two mortgages is paid to you in cash, which you can then use to purchase a larger home. Cash-out refinances can be either fixed-rate or adjustable-rate mortgages (ARMs).

What do the numbers look like?

The amount of money you can borrow using either of these methods will depend on your home's equity and your credit score.

Here is an example of how you could use a home equity loan to buy a larger home if your current home is worth $1,500,000:

- Your current home is worth $1,500,000 and you have a $1,000,000 mortgage, so you have $500,000 in equity.

- You find a larger home that you want to buy for $2,000,000.

- You take out a home equity loan for $400,000.

- You use the $400,000 from the home equity loan and a $1,600,000 mortgage to buy the larger home.

In this example, you were able to use your home equity to make a 20% down payment on the larger home, which helped you qualify for a lower interest rate on your mortgage.

It is important to note that this is just an example and the actual amount of money you can borrow will depend on your individual circumstances, such as your credit score and debt-to-income ratio.

Here are some additional things to consider when using a home equity loan to buy a larger home:

- Interest rates: Home equity loans typically have lower interest rates than other types of loans, such as personal loans or credit cards. However, it is important to compare rates from different lenders to get the best deal.

- Closing costs: There are closing costs associated with taking out a home equity loan, which can range from 2% to 5% of the loan amount. Be sure to factor these costs into your budget.

- Repayment terms: Home equity loans typically have repayment terms of 5 to 30 years. It is important to choose a term that you can afford and that will allow you to pay off the loan in a timely manner.

Overall, using a home equity loan to buy a larger home can be a good option if you have enough equity in your current home and you can afford the monthly payments. However, it is important to weigh the risks and benefits carefully before making a decision.

How To Find Out How Much Equity You Have

The best way to learn how much you have is to reach out to a trusted real estate agent for a Professional Equity Assessment Report (PEAR).

Bottom Line

If you’re planning to make a move, the equity you’ve gained can make a big impact. To find out just how much equity you have in your current home and how you can use it to fuel your next purchase, let’s connect.

Categories

Recent Posts

GET MORE INFORMATION