The Ripple Effect: How Interest Rates Shape Institutional Real Estate in 2026

The Ripple Effect: How Interest Rates Shape Institutional Real Estate in 2026

Institutional real estate—encompassing office towers, logistics parks, multifamily complexes, retail centers, and specialized assets like data centers held by pension funds, insurance companies, sovereign wealth funds, and REITs—has long served as a cornerstone of diversified portfolios. Its performance is inextricably linked to interest rates through borrowing costs, valuation mechanics, investor demand, and capital allocation decisions.

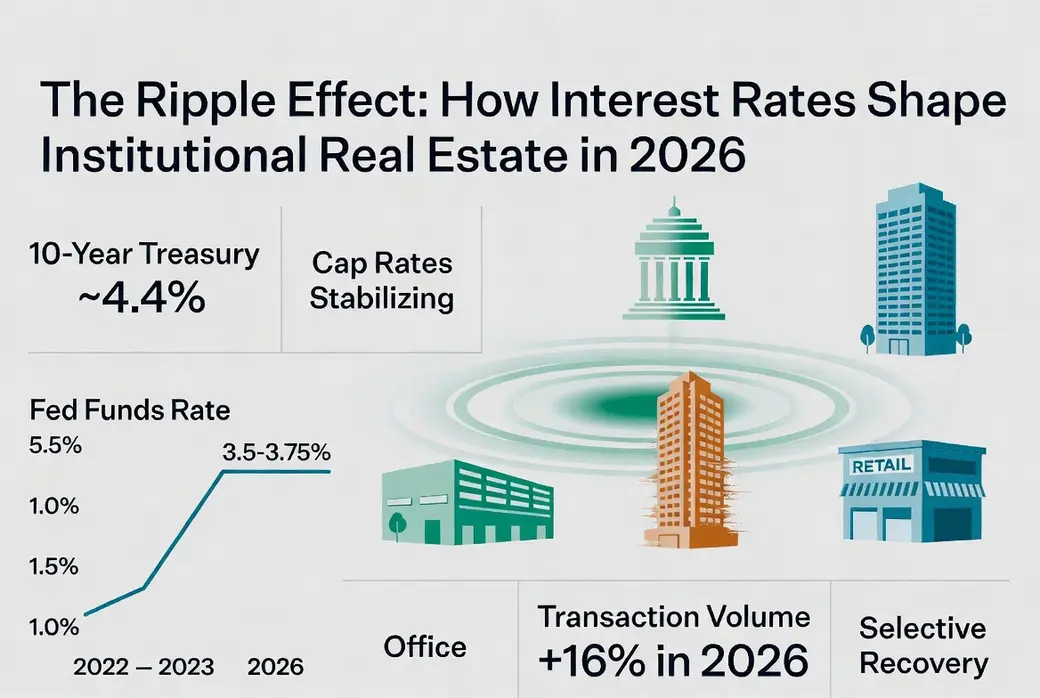

As of May 2026, with the Federal Funds rate stabilized in the 3.50–3.75% range and the 10-year Treasury yield hovering around 4.4%, the sector is navigating the aftermath of the sharp 2022–2024 rate-hike cycle and entering a phase of stabilization and selective recovery.

The Core Mechanics: How Interest Rates Drive Real Estate Dynamics

Interest rates influence institutional real estate through several interconnected channels:

- Cost of Capital and Discount Rates: Higher rates raise the discount rate applied to future net operating income (NOI) in discounted cash flow models, directly lowering present values and property prices. A 100-basis-point rise in rates can compress values by 10–15% or more, all else equal.

- Capitalization (Cap) Rates: These risk-adjusted yields (NOI divided by property value) typically expand when risk-free rates (e.g., 10-year Treasuries) rise, as investors demand higher returns to compensate for elevated financing costs and opportunity costs versus bonds. Conversely, falling or stable rates support cap rate compression and value appreciation.

- Debt Financing and Refinancing: Real estate is highly leveraged. Rising rates increase debt service, strain debt-service coverage ratios (DSCR), and complicate refinancing of maturing loans—particularly those originated at sub-4% rates during the 2020–2021 low-rate era. When all-in borrowing costs exceed cap rates (a dynamic seen in 2023–early 2025), leverage becomes dilutive rather than accretive.

- Investor Competition and Flows: Higher bond yields make fixed-income alternatives more attractive, reducing capital chasing real estate. Lower rates reverse this, boosting demand for real estate’s income and inflation-hedging qualities. Institutions also rebalance portfolios: real estate’s correlation with equities and bonds shifts with rate regimes.

- Supply and Fundamentals: Elevated construction financing costs slow new development, eventually tightening supply and supporting rents—but only after a lag. Demand-side effects vary by sector (e.g., e-commerce-driven logistics vs. hybrid-work office).

These mechanisms explain why the 2022–2023 Fed hiking cycle triggered one of the most significant valuation resets in decades.

From Boom to Repricing: 2022–2025 Context

The ultra-low rate environment of 2020–2021 fueled aggressive cap rate compression (often below 4–5% in prime assets), record transaction volumes, and heavy institutional allocations. Property values soared on cheap debt and yield-chasing.

The Fed’s aggressive tightening—lifting the funds rate from near-zero to over 5.25% by mid-2023—reversed this dramatically. Transaction volumes plummeted (down ~70% in early periods for some segments), cap rates expanded sharply (industrial from ~4% lows toward 6%+ in places), and values declined 15–30% in many markets.

By 2025, the repricing cycle largely concluded. Cap rates stabilized, with industrial assets showing mid-year compression (to ~5.5%) before a Q4 2025 snapback to ~6.4% as broader deal flow resumed. Lending activity rebounded (up 45% YoY in Q2 2025), and equity fundraising improved. Institutions began viewing the reset as creating attractive entry points, especially versus still-elevated bond yields.

2026 Landscape: Stabilization with Dispersion

Entering 2026, the environment is more constructive but far from uniform. The Fed has delivered measured cuts since late 2024, bringing the policy rate to ~3.5–3.75%, with further modest easing anticipated toward a 3.0–3.25% terminal range. The 10-year Treasury remains anchored near 4.4%, providing a stable (if elevated versus pre-2022) backdrop.

Key developments include:

- Cap Rate Outlook: Most property types are past their cyclical peaks. Modest compression of 5–15 bps is expected in 2026 for industrial, multifamily, and necessity retail, assuming contained rate volatility. Office and secondary assets face stickier (higher) cap rates due to structural risks.

- Transaction Recovery: Investment activity is forecast to rise ~16% in the U.S. to ~$562 billion, approaching pre-pandemic averages, supported by narrowing bid-ask spreads and normalizing debt costs (now often aligned with or below cap rates).

- Income Over Valuation: With limited scope for broad cap rate compression, total returns will increasingly derive from NOI growth (projected 3–6% in many sectors) rather than multiple expansion.

Institutional sentiment has turned cautiously optimistic. Target real estate allocations dipped slightly in 2025 (first decline in 13 years, to ~10.7%) amid competition from infrastructure and private credit, yet institutions remain meaningfully under-allocated (~90 bps gap). Many plan to increase commitments in 2026 as valuations bottom and liquidity improves.

Sector-Specific Impacts

Performance diverges sharply by property type:

- Industrial/Logistics & Data Centers: Most resilient. Strong e-commerce, supply-chain, and AI-driven demand support robust rent growth and occupancy. Cap rates have largely completed repricing; modest compression is plausible in 2026. Flight-to-quality favors Class A assets.

- Multifamily: Demographics remain supportive long-term, but a supply wave in certain markets has pressured rents and occupancy. Rate sensitivity is high via tenant affordability. Class A assets in supply-constrained markets fare best; cap rates around 4.7–5.4% depending on class.

- Office: Most challenged. Hybrid work, elevated vacancies, and higher risk premiums keep cap rates elevated (8.4%+ for Class A). Values have declined significantly; recovery will be slow and selective (prime CBD or amenity-rich assets). Distress opportunities exist but require careful underwriting.

- Retail: Necessity-based and grocery-anchored properties demonstrate stability. Experiential and mall formats remain mixed. Overall, retail has outperformed broader CRE in the rate-reset period.

- Specialty (Healthcare, Self-Storage, Hotels): Vary widely; healthcare and self-storage often exhibit lower rate sensitivity due to inelastic demand.

REITs, as liquid proxies for institutional real estate, have shown resilience. U.S. REITs delivered modest 2025 returns (~2.3%) but posted strong early 2026 performance (~6%+ YTD through mid-March) as rates stabilized and operational fundamentals (FFO growth) shone. Their lower historical debt costs (~4.1% weighted average) and high payout ratios position them well for any further easing.

Institutional Strategies in the New Environment

Leading institutions are adapting with:

- Selectivity and Dispersion Focus: Broad “rising tide” strategies no longer work. Emphasis on asset-level fundamentals, market selection, and active management.

- Income Prioritization: Underwriting assumes higher exit cap rates and stresses cash-flow growth over yield compression.

- Capital Structure Optimization: Opportunistic refinancing, preferred equity, or recapitalizations where debt costs normalize.

- Portfolio Integration: Increased use of REITs for liquidity, diversification, and exposure to growth sectors (data centers, life sciences). Many pensions now allocate 70%+ of real estate exposure via public vehicles alongside private.

- Global and Thematic Tilts: Greater interest in Europe (improving fundamentals) and Asia, plus thematic bets on AI infrastructure and demographics.

Risks remain: sticky inflation could delay further cuts; policy uncertainty (tariffs, fiscal shifts) adds volatility; and sector-specific oversupply or obsolescence could prolong pain in offices or certain multifamily submarkets.

Outlook and Key Takeaways for 2026–2027

The higher-for-longer rate regime has permanently altered the landscape: gone are the days of easy cap rate compression and cheap leverage driving returns. Success now hinges on operational excellence, disciplined capital allocation, and positioning in structurally advantaged sectors.

For institutional investors, 2026 offers a window of opportunity. Stabilizing rates, recovering transaction volumes, and attractive relative yields versus bonds create conditions for renewed capital deployment—provided selectivity prevails. Those who treat real estate as a cash-flow business rather than a beta play on rates will likely outperform.

The era of rate-driven volatility has given way to one of fundamentals-driven dispersion. Institutions that navigate this shift with precision stand to capture compelling risk-adjusted returns in the years ahead.

This analysis draws on market data and outlooks as of early May 2026. Real estate decisions should incorporate professional advice tailored to specific portfolios and risk tolerances.

Categories

Recent Posts

GET MORE INFORMATION