"Golden Handcuffs” of Low Mortgage Rates

Nearly Half of Americans Feel Trapped by “Golden Handcuffs” of Low Mortgage Rates

The American dream is facing a new kind of constraint — one not driven by affordability alone, but by the invisible shackles of historically low mortgage rates. According to Storable’s 2026 Moving Forecast, 46% of U.S. homeowners say they feel trapped in their homes, unwilling to sell or relocate for fear of losing their low monthly payments.

Here I explore this concept and what effect this might have on home prices.

The Power of the Rate Lock-In

In the wake of the COVID-era housing boom, millions of Americans secured 30-year mortgages below 4%. Today, with rates hovering near 6%, those loans have turned into golden handcuffs. Homeowners are holding tight to rates they may never see again — and the numbers show just how anchored they’ve become.

Among homeowners with a mortgage, 73% said they would move if they could transfer their current rate to a new property. Nearly one in three said they would do so immediately. But because current lending systems don’t allow portability, most remain stationary, even if life or career changes beckon elsewhere.

Golden Handcuffs Tighten

The emotional and financial attachment to those low payments runs deep. One in four homeowners with rates below 5% said no amount of money could convince them to give up their current mortgage. Another 24% said it would take a financial incentive of at least $200,000.

When asked what mortgage rate would make them seriously consider moving, 38% said rates would have to drop below 4.5%, with another 17% saying between 4.5% and 5%. With Freddie Mac’s 30-year average stuck near 6%, it’s little wonder housing mobility remains frozen.

And that immobility has ripple effects:

-

56% have turned down or would turn down a job requiring relocation.

-

33% have stayed in a relationship or living situation longer than they wanted due to financial constraints.

-

41% have rented or considered renting storage because they need more space but can’t afford a larger home.

A Market Slowly Thawing

There are faint signs of movement. For the first time in late 2025, the share of U.S. mortgages above 6% surpassed those below 3%, according to Realtor.com — suggesting that newer buyers, though smaller in number, may help the market slowly rebalance. Still, about 80% of mortgage holders are locked in below 6%, keeping supply tight and home prices stubbornly high.

Renters, meanwhile, are losing confidence. One in four say they will probably never own a home, and 21% have abandoned the goal altogether. This growing pessimism poses long-term challenges for generational wealth building and workforce flexibility.

Searching for Solutions

Policymakers are beginning to explore ideas once considered exotic, such as portable mortgage rates that allow homeowners to carry their existing loan terms to a new home. The Federal Housing Finance Agency has reportedly begun studying such options, though implementation could still be years away.

In the meantime, industries like self-storage are becoming unexpected beneficiaries of this gridlock. As homeowners stay put but outgrow their space, they’re renting storage units instead of upsizing — a small but telling adaptation to an immovable housing system.

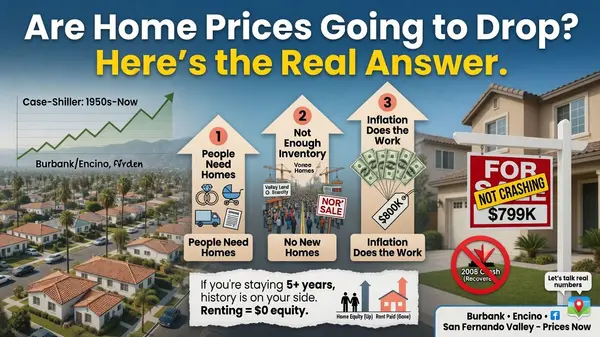

What this means for home prices

You can add a section that explains how rate lock-in props up prices now, and what might happen as the market slowly thaws.

How Mortgage Lock-In Shapes Home Prices

The same “golden handcuffs” keeping people in place are also keeping home prices higher than they otherwise would be. When millions of owners refuse to sell because they do not want to trade a 3–4% mortgage for something near 6%, the number of homes for sale shrinks, even if demand cools a bit. Economists estimate that this lock-in driven reduction in moves has boosted home values by roughly 7–8% nationally in recent years, largely offsetting the normal downward pressure higher rates would put on prices.fhfa+1

In practical terms, the lock-in effect acts like a lid on inventory and a cushion under prices. Even as listings have increased from their pandemic lows, national median list prices remain significantly higher than a few years ago because there are still more motivated buyers than willing sellers in many markets. That imbalance lets sellers hold firm on asking prices, and forces buyers—especially those moving out of necessity—to stretch further than they expected.

Over time, as more homeowners with ultra-low rates are replaced by buyers with 5–6% loans, the market is expected to “recalibrate.” Analysts see signs that the lock-in effect is slowly easing as the share of mortgages above 6% grows and rates drift down modestly, but they do not expect a broad price crash. Instead, most forecasts call for flat to modestly rising prices nationally, with any price softness showing up mainly in overheated or highly rate-sensitive metros.nationalmortgageprofessional+2

For local markets, the impact will be uneven. High-cost coastal areas, where the payment difference between a 3% and 6% mortgage is enormous, may stay inventory-starved and price-resilient longer. More affordable regions with less severe lock-in could see a quicker normalization: slightly more listings, a bit more negotiation room for buyers, and slower—but still positive—price growth rather than double-digit appreciation.kiplinger+2

For L.A.-area homeowners, these dynamics are especially important. Lock-in is likely to keep inventory tighter than normal and continue supporting prices, particularly in desirable neighborhoods where many owners hold sub-4% loans. At the same time, any meaningful drop in mortgage rates could quickly unlock years of pent-up move-up demand, creating a short window where more listings hit the market, buyers have more choices, and well-prepared sellers can still achieve strong prices while successfully making their next move.

Would you like me to tailor this article for publication on your real estate blog, perhaps by adding a short introduction and closing call-to-action aimed at homeowners in the Los Angeles market?

Categories

Recent Posts

GET MORE INFORMATION